With all the different costs associated with Medicare, you may be wondering how excess charges apply to you and your situation.

An excess charge is an amount your provider bills when they do not accept Medicare-approved payment amounts as payment in full. Excess charges are billed for outpatient services only and do not satisfy the yearly Medicare Part B deductible. The charge cannot be more than 15% of the Medicare-approved amount. The Medicare Overcharge Measure does not allow providers in certain states to bill excess charges.

It is essential to understand what these costs are and how to avoid them.

Keep reading to learn more.

Why Do Some Providers Not Accept Medicare Assignment?

Sometimes there are providers who choose not to accept Medicare beneficiaries as patients. Usually, this happens if a provider stays busy enough to not need additional business, something that is happening more and more frequently.

You can find yourself in a situation with higher out-of-pocket costs if you are not careful.

If you go to a doctor that does not accept Medicare, you’ll end up paying the entire amount.

With lower reimbursement rates, providers are choosing to refuse Medicare including more and more specialty doctors.

In order to maintain a large range of different services available, Medicare allows providers to bill more than what the Medicare-approved amounts are.

This gives you more choices when picking a provider.

If you have treatment with a doctor that does not accept Medicare assignment, they’ll bill up to 15% of the Medicare-approved amount, as mentioned above.

The good news is that on average, 96% of all providers accept Medicare assignment as payment in full.

When Are Excess Charges Billed?

The chance of you having an excess charge is pretty small.

If you see a provider that does bill them, they usually collect this amount upfront in the form of a copay.

The average cost of an excess charge is less than $20. This is good news. It means something to not worry about – most of the time.

The charge though does not count towards any deductible or copays that you may owe.

Sometimes providers bill Part B even if you are in the hospital.

As you know, Part A covers all in-patient hospital stays, but depending on the service, Part B may be billed also.

The problem here is that if you’re hospitalized, bills are typically significantly higher. So if you end up getting a charge in the hospital, it definitely will be more than $20.

The good news is you can protect yourself from excess charges. We’ll talk about this more below.

Excess Charges & Part B

Providers can only bill for excess charges if Part B covers the service.

Part B is outpatient medical coverage for services such as visits to doctors and specialists. You can read more about Part B here.

Hospital admissions typically do not have excess charges (Part A).

Part A is inpatient hospital coverage for services associated with hospital admissions. You can read more about Part A here.

It is important to note that being in the hospital and receiving services in a hospital setting does not necessarily mean that visits and those services fall under Part A.

Sometimes services covered by Part B are performed in a hospital setting.

Hospitals are more likely to charge an excess charge if they bill Part B.

Here’s an example as it relates to Part B (inpatient):

Greg scheduled his gallbladder removal surgery in the hospital ahead of time.

He is not admitted and is home the same day.

Part B covered his surgery.

If a provider, who does not accept assignment, treated him, that provider might bill him for excess charges.

Another example, this time for Part A (outpatient):

Susan recently had a heart attack and learned that she needed bypass surgery.

She is admitted to the hospital for the surgery and spends the better part of a week there.

Because she was admitted and considered an inpatient, Part A covers her services.

She is not subject to any excess charges.

If the surgery is done outpatient (even though she was admitted and might not know any different), the hospital may still charge an access charge for the procedure.

Why Do Some Doctors Not Accept Assignment?

Earlier I mentioned that some doctors do not accept Medicare at all while others may accept Medicare, but not Medicare assignment.

There are 3 types of contracts providers participate in:

- PAR Provider – Those that accept Medicare as payment in full

- Non-PAR Provider – Doctors and hospitals that take Medicare, but may charge an excess fee

- Private Contract – Providers that do not take Medicare at all (they may take Medicare Advantage)

From what we’ve seen, the reason why Medicare allows physicians to have a contract even though they have higher fees is that Medicare needs there to be more specialists available to choose from. Very rarely do we see primary care physicians not accept assignment. The most common are specialists that may charge a bit more.

How to Avoid Access Charges

There are 3 ways to avoid paying access charges.

- Go to a PAR Provider – one that accepts Medicare Payment as Payment in full

- Get a Medicare Supplement

- Get a Medicare Advantage Plan

Let’s talk about each one of these briefly.

Go to a Provider That Accepts Medicare Assignment

This one is pretty straightforward.

If you want to avoid these higher charges, go to a doctor or specialist that is a PAR-provider. You can see which doctors accept Medicare assignment by using Medicare’s Provider search tool. You can find it here.

Chances are though, your current primary care physician does accept Medicare as payment in full.

Let’s look at an example:

Dr. Smith charges $300 per visit at his practice.

His office accepts Medicare patients and accepts assignment.

Medicare is willing to pay $150 for the cost of an office visit at Dr. Smith’s office.

Because Dr. Smith accepts assignment, he agrees to the $150 as payment in full, and no one is responsible for any additional amount above that.

Get a Supplement

Medicare Supplements are a great way to lower out-of-pocket costs. They allow you to keep Medicare as your primary insurance while covering expenses that Medicare would normally pass down to you. Read more about Supplement plans Here.

Some Medicare Supplements pay the Part B Excess charges so you don’t have to. If excess charges are a concern, remember to ask your agent to show you plans that include these benefits.

Now, the thing to remember is that not all Medicare Supplements cover excess charges.

As you’ll soon learn, some states passed a law that makes it illegal for providers to charge more than the Medicare Approved amount.

This law was called the Medicare Overcharge Measure.

So, naturally buying a Supplement that has these benefits included would not be a good fit.

If you want to know more about the different Medicare Supplements, you can learn about them here.

Let’s look at an example:

Christopher has a Plan N Medicare Supplement in addition to Part A and Part B.

Plan N does not cover excess charges.

Christopher visits a psychologist who sees Medicare patients but does not accept the assignment.

The psychologist charges $200 for a visit, but Medicare approves only $100.

In addition to the standard $20 copay for office visits on Plan N, Christopher also receives a $15 excess charge bill.

As you can see, the excess charge is 15% of the Medicare-approved amount of $100 and not 15% of the psychologist’s standard rate of $200.

An excess charge will always be a maximum of 15% of the Medicare-approved amount and not of the total amount the provider typically charges.

Get a Medicare Advantage Plan

As we’ve talked about before, Advantage Plans are an alternative to Medicare.

You have the option of going with a plan that has its own set of networks and restrictions instead of going with original Medicare. Read more about that here.

If your current provider does not accept Medicare, they may take Medicare Advantage Plans.

When buying an Advantage Plan, you’ll be able to see if your current doctor is in the plan’s network. The good news is that you can usually see this information before you buy.

If your current provider does not accept Medicare as payment and full, there may be Advantage Plans available the satisfy the amount the doctor is billing.

All this is information your agent can go over.

If you do not have an agent you are working with, you can learn how to pick one here.

What is Medicare Overcharge Measure?

In short, some states made it illegal for providers to charge more than the Medicare Approved amount.

Physicians only have a choice to participate in Medicare’s network, or opt-out.

If a provider decides to not take Medicare at all, they cannot file any claims to Medicare for 2 years.

It is illegal in the following states for providers to bill for excess charges:

- Connecticut

- Massachusetts

- Minnesota

- New York

- Ohio

- Pennsylvania

- Rhode Island

- Vermont

Suppose you are considering a Medicare Supplement as additional coverage and live in one of these states. There are plans available that do not cover excess charges. You can save money on the premiums by going this route, and not worry about excess charges.

A Medicare Supplement that does not cover access charges typically costs less. You can read more about these plans here.

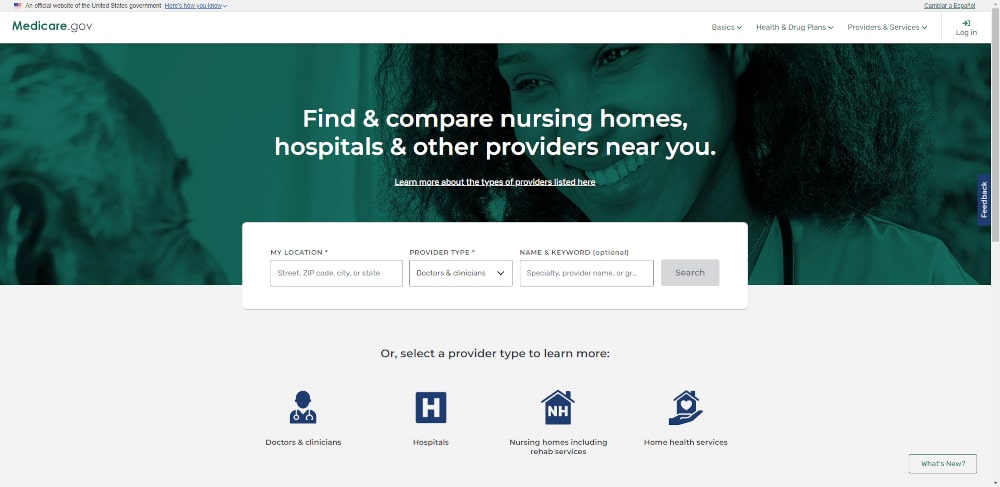

Finding a Doctor: Step by Step

Let’s say you have only Original Medicare and a Supplement that does not cover excess charges.

We mentioned above that it is best to look into whether your provider accepts assignment. Here is the link again.

To find a doctor follow these simple steps:

- Enter the city and state or zip code

- Enter the name of a provider, group, or area of medical specialty (for example, cardiology, orthopedics, pulmonology, etc.)

- Hit the search button

Your search should yield a page of results.

Next to the provider or group name, you should see a green checkmark, and beside it, the words “accepts Medicare-approved payment amounts.”

If you see this, you know that this provider or group accepts the assignment and will not bill you for any excess charges.

Summary

You could potentially be subject to excess charges on Medicare if you see a healthcare provider who does not accept the assignment.

The good news is that most providers do.

You can always use the link above to verify.

The average excess charge is less than $20 and they are typically pretty minimal when providers bill for them.

The best way to avoid excess charges if you do not have Medicare supplement Plan F or Plan G is to determine whether a provider accepts assignment before visiting him or her.

If you have any questions, use the search tool at the top of this page or on the home page.

Or, if you would like further detail on any of the topics we discussed, please fill out a contact form and submit your question.

If you prefer to speak by phone, call us at 888-209-5049.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment